Texas First-Time Homebuyer Programs: Your Complete 2026 Guide

Texas is one of the best states in the country to be a first-time buyer. Between statewide assistance programs, city-specific grants, and federal loan options, there's more help available than most people realize.

This guide breaks down everything you need to know: the real numbers, the programs that can lower your costs, and the step-by-step path to getting your keys.

What Does "First-Time Homebuyer" Actually Mean in Texas?

Before we dive into programs, let's clear up a common misconception. You don't have to be a first-time buyer in the literal sense to qualify for most of these programs.

In Texas, and under the federal HUD definition used by most assistance programs, a "first-time homebuyer" is anyone who has not owned a primary residence in the past three years. That means if you owned a home five years ago, sold it, and have been renting since, you likely qualify.

This opens the door for a lot more Texans than most people expect.

The Texas Housing Market in 2026: What You're Working With

Here's a snapshot of the current market so you know what you're entering:

- Median home price in Texas: approximately $330,000 (December 2025)

- 30-year fixed mortgage rate: around 6% in early 2026

- Typical 5% down payment: approximately $16,500

- Average Texas credit score: 692 (Experian, 2025)

- Home sales trend: up 6.1% year-over-year as of December 2025

The market has stabilized after several years of rapid appreciation. Inventory is improving in many suburbs and smaller cities, meaning buyers have more options and slightly more negotiating room than they did two or three years ago.

San Antonio, in particular, offers a strong mix of affordability and job growth, one of the best markets in the state for first-time buyers.

The Biggest Myth: You Need 20% Down

This is the #1 reason first-time buyers delay purchasing, and it's simply not true.

On a $330,000 Texas home, here's what your actual minimum down payment looks like by loan type:

Loan Type | Minimum Down Payment | On a $330K Home

-VA Loan | 0% | $0 |

-USDA Loan | 0% | $0 |

-FHA Loan | 3.5% | $11,550 |

-Conventional | 3% | $9,900 |

And with Texas assistance programs, even those amounts may be covered for you.

Texas First-Time Homebuyer Programs: The Full Breakdown

1. Texas State Affordable Housing Corporation (TSAHC)

TSAHC is one of the most accessible statewide programs for Texas buyers. Here's what they offer:

Down Payment Assistance (DPA)

TSAHC provides grants and forgivable loans to cover your down payment and closing costs. To qualify, you generally need:

- A credit score of 620 or higher

- Income within program limits (varies by county and household size)

- Purchase of a primary residence

The assistance can be structured as a grant (no repayment required) or a second lien with deferred or forgivable terms.

Homes for Texas Heroes

If you work in public service, including teachers, police officers, firefighters, EMS personnel, correctional officers, or veterans, you may qualify for the Homes for Texas Heroes program, which offers below-market interest rates and down payment assistance specifically for these professions.

2. Texas Department of Housing & Community Affairs (TDHCA)

TDHCA administers two major programs for Texas buyers:

My First Texas Home

This program offers 30-year, fixed-rate mortgages at below-market rates combined with down payment and closing cost assistance. It's specifically for first-time buyers (or those who haven't owned a home in three years) and has income limits based on your area.

My Choice Texas Home

This is the same benefit structure but without the first-time buyer requirement. It has higher income limits, making it available to more households. It's a great option if you previously owned a home and don't technically qualify for first-time programs.

Both programs also allow you to combine assistance with a Mortgage Credit Certificate (MCC)—more on that below.

3. Mortgage Credit Certificate (MCC) Program

The MCC is a federal tax credit that gives first-time buyers a credit of up to 15% of the mortgage interest they pay each year, directly reducing their federal tax bill, not just their taxable income.

Here's a simple example of how it works:

- You pay $12,000 in mortgage interest in year one

- 15% of that = $1,800 tax credit

- That $1,800 comes directly off your federal taxes owed

Over the life of a 30-year mortgage, this can add up to tens of thousands of dollars in savings. The MCC can be combined with down payment assistance programs, making it one of the most powerful tools available to Texas first-time buyers.

Check with your lender to confirm current availability and eligibility, as program funding and rules can change.

4. City-Specific Down Payment Assistance Programs

Beyond statewide programs, many Texas cities offer their own assistance, sometimes layered on top of TSAHC or TDHCA benefits.

San Antonio — Homeowner Incentive Program (HIP) San Antonio offers assistance for qualifying buyers purchasing within city limits. Contact the city's Neighborhood & Housing Services Department for current funding availability and income requirements.

Houston — Homebuyer Assistance Program (HAP) Houston offers up to $50,000 in down payment and closing cost assistance for income-qualified buyers. The assistance is structured as a no-interest, forgivable loan — meaning if you live in the home for five years, the loan is fully forgiven.

Dallas — Dallas Homebuyer Assistance Program (DHAP)Dallas also offers up to $50,000 in assistance, structured as a forgivable deferred loan with no monthly payments and no interest. Income limits apply (at or below 80% of area median income).

Other Texas cities with DPA programs include Arlington, Austin, Beaumont, Bryan, Denton, and Texarkana.

Federal Loan Options for Texas First-Time Buyers

In addition to state programs, first-time buyers in Texas have access to several federal loan types that offer lower barriers to entry:

FHA Loans

Backed by the Federal Housing Administration, FHA loans offer:

- Down payments as low as 3.5%

- Credit score minimums starting around 580

- Flexible debt-to-income guidelines

FHA loans are one of the most common choices for first-time buyers and can be combined with Texas DPA programs.

VA Loans

For active-duty military, veterans, and eligible surviving spouses, VA loans offer:

- Zero down payment

- No private mortgage insurance (PMI)

- Competitive interest rates

- Flexible qualifying criteria

San Antonio, as a home to major military installations, has a large population that qualifies for VA loans. At TLP Mortgage, helping military families navigate VA benefits is something our team does every day.

USDA Loans

For buyers purchasing in eligible rural and some suburban areas, USDA loans offer zero down payment and reduced mortgage insurance costs. Parts of the greater San Antonio and Texas Hill Country areas may qualify.

Conventional Loans

With as little as 3% down, conventional loans are a strong option for buyers with good credit (typically 620+). Once you reach 20% equity, private mortgage insurance (PMI) can be removed.

What Does Closing Cost Assistance Look Like?

A down payment is only part of the upfront cost. Closing costs, which cover things like appraisal, title insurance, lender fees, and prepaid expenses, typically run 2–5% of the purchase price.

On a $330,000 home, that's $6,600 to $16,500 in additional costs due at closing.

Many of the programs listed above cover closing costs in addition to the down payment. This is a significant benefit that buyers often overlook when comparing their options.

Your Credit Score: The Real Numbers

Many buyers assume they need a perfect credit score. Here's what the data actually shows:

- FHA loans: minimum 580 for 3.5% down (500–579 may qualify with 10% down)

- Conventional loans: typically 620 minimum

- TSAHC programs: 620 minimum

- VA and USDA loans: no official minimum, though most lenders look for 580–620+

- Average Texas credit score: 692 — well within qualifying range for most programs

If your score needs work, that's okay. Steps like paying down revolving balances, disputing errors on your credit report, and avoiding new credit inquiries can move your score meaningfully in 3–6 months. A good loan officer will walk you through a credit improvement plan before you apply.

The 10-Step Path to Buying Your First Texas Home

1. Check your credit: Pull your free reports at annualcreditreport.com. Know what you're working with before anything else.

2. Set your budget: Factor in down payment, closing costs, monthly payment, insurance, and property taxes. Texas property taxes are higher than the national average, so don't skip this step.

3. Connect with a loan officer: Before you look at a single house, get pre-qualified. This tells you exactly what you can afford and strengthens your offer.

4. Explore assistance programs: Your loan officer can identify which state, city, and federal programs you qualify for before you apply.

5. Get pre-approved: Pre-approval is stronger than pre-qualification and requires full documentation (see checklist below).

6. Find a real estate agent: Work with a local agent who knows your target neighborhoods.

7. Shop for homes: With a pre-approval letter in hand, you're a serious buyer.

8. Make an offer: Your agent guides the negotiation. Your lender is in the background keeping your financing on track.

9. Home inspection and appraisal: Protect yourself with an inspection. The lender will order an appraisal to confirm the home's value.

10. Close: You'll sign your final loan documents, pay any remaining closing costs, and receive your keys.

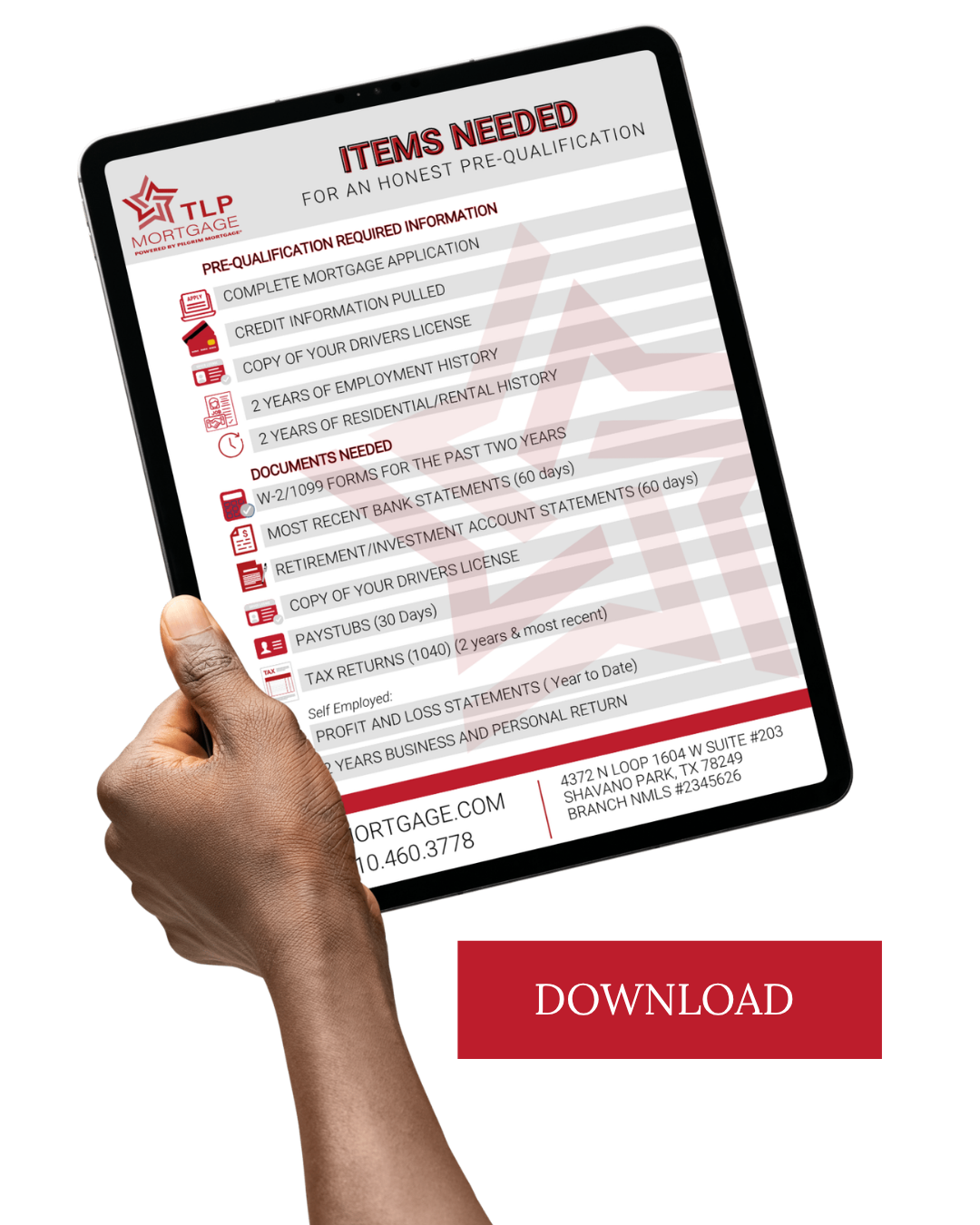

Documents to Gather Before You Apply

Getting these ready in advance makes the process dramatically faster:

- Last two years of W-2s (or 1099s if self-employed)

- Last 30 days of pay stubs

- Last two months of bank statements (all accounts)

- Last two years of federal tax returns

- Government-issued photo ID

- Social Security number

Why TLP Mortgage for Your First Home?

At TLP Mortgage, powered by Pilgrim Mortgage®, we've made it our mission to guide first-time buyers through every stage of the process, not just process a loan.

Our team includes loan officers who specialize in VA loans, down payment assistance programs, construction loans, and the TX Vet Program. We're based in Shavano Park, right in the heart of San Antonio, and we work with buyers across Texas.

We'll review your financial picture, identify every program you qualify for, and build a strategy tailored to your goals. Whether you're ready to buy now or planning for 12 months from now, we'd love to connect.

Ready to Find Out What You Qualify For?

The first step is easier than you think. Use TLP's pre-qualification checklist to gather your documents, then connect with one of our loan advisors for a free, no-obligation consultation.